28 significance (p-value)

Given a correlation coefficient r, we can assess its significance using a p-value. Let’s formulate the hypotheses:

- Null Hypothesis (H_0): There is no correlation between the two variables (i.e., r = 0).

- Alternative Hypothesis (H_a): There is a correlation between the two variables (i.e., r \neq 0).

To calculate the p-value, we can use the following formula for the test statistic t:

t = \frac{r \sqrt{n - 2}}{\sqrt{1 - r^2}} \tag{1} where n is the number of data points.

This formula follows the fundamental structure of a t-statistic:

t = \frac{\text{Signal}}{\text{Noise}} = \frac{\text{Observed Statistic} - \text{Null Value}}{\text{Standard Error of the Statistic}} \tag{2}

Let’s rearrange Eq. (1) to match the structure of Eq. (2):

t = \frac{r - 0}{\sqrt{\frac{1 - r^2}{n - 2}}} \tag{3}

The numerator is clear enough. Let’s discuss the denominator, which represents the standard error of the correlation coefficient.

The term 1 - r^2 is the proportion of unexplained variance in the data. As the correlation r gets stronger (closer to 1 or -1), the unexplained variance gets smaller. This makes intuitive sense: a very strong correlation is less likely to be a result of random chance, so the standard error (noise) should be smaller.

The term n−2 is the degrees of freedom. As your sample size n increases, the denominator gets larger, which makes the overall standard error smaller. This also makes sense: a correlation found in a large sample is more reliable and less likely to be a fluke than the same correlation found in a small sample.

Let’s try a concrete example.

calculate a bunch of stuff

# compute sample z-scores of x, y

zx = (x - np.mean(x)) / np.std(x, ddof=0)

zy = (y - np.mean(y)) / np.std(y, ddof=0)

# compute Pearson correlation coefficient

rho = np.sum(zx * zy) / N

# compute t-statistic

t = rho * np.sqrt((N-2) / (1-rho**2))

# compute two-sided p-value

p = 2 * (1 - stats.t.cdf(np.abs(t), df=N-2))plot

fig, ax = plt.subplots(1, 1, figsize=(5, 5))

ax.scatter(x, y, label='data', alpha=0.5)

# linear fit and R2 with scipy

slope, intercept, r_value, p_value, std_err = stats.linregress(x, y)

ax.plot(x, slope*x + intercept, color='red', label=f'linear regression, R²={r_value**2:.2f}')

ax.legend(frameon=False)

# print p-value

print(f'our p-value: {p:.4f}')

print(f'scipy p-value: {p_value:.4f}')

# compute correlation coefficients and their p-values

r = np.corrcoef(x, y)[0,1]

ax.set(xlabel='x',

ylabel='y',

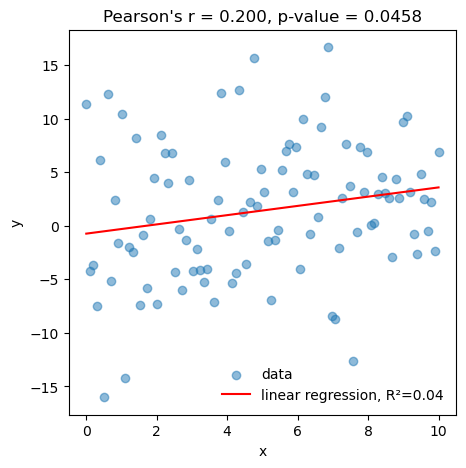

title=f"Pearson's r = {rho:.3f}, p-value = {p_value:.4f}");our p-value: 0.0458

scipy p-value: 0.0458

The linear regression accounts for 4% of the variance in the data, which corresponds to a correlation coefficient of r = 0.2. This correlation is statistically significant at p=0.0458<0.05.